The Canadian Property & Casualty (P&C) insurance industry capped off 2024 with another quarter of robust financial performance. Based on data reported to OSFI under IFRS 17 standards, the sector posted year-to-date revenues of $86.94 billion, up from $75.30 billion in the same period last year, a 15% year-over-year increase.

Despite strong top-line growth, net profits after tax slightly declined by 1%, decreasing from $9.58 billion in 2023 to $9.47 billion in 2024. Net income, however, modestly increased by 1%, moving from $9.48 billion last year to $9.54 billion in 2024. This indicates that, while the industry achieved significant revenue growth, rising service expenses, up 26% year-over-year, put pressure on overall profitability.

Market Leaders and Key Highlights

-

Intact Financial Corporation remained the top revenue generator with $12.1 billion in 2024 revenue, maintaining its stronghold at the top of Canada’s P&C sector.

-

Lloyd’s Underwriters led in profitability once again, reporting $2.81 billion in net income. Their consistent underwriting performance and global scale continue to make them a dominant force in the Canadian market.

-

Aviva Canada and Co-operators General followed closely in total revenue, reinforcing their positions as top-tier players in the domestic space.

-

Definity Financial, Wawanesa Mutual, and Aviva Canada posted strong results across both revenue and income, highlighting their operational resilience and steady growth.

-

Several mid-tier companies — including Certa, Northbridge, and Chubb Canada — also secured spots in the top 20 by revenue, reflecting a healthy mix of large incumbents and agile challengers.

-

The data illustrates a diversified market, with both domestic and foreign insurers contributing meaningfully to overall growth, suggesting competitive momentum across all segments.

Top 20 by Revenue

Fastest Growing by Revenue

The following companies showed standout year-over-year revenue growth:

-

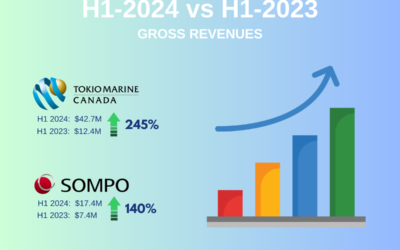

Tokio Marine Canada Ltd.: 245.5% growth, rising from $23.6 million in 2023 to $81.5 million in 2024.

-

Sompo Japan Insurance Inc.: 151.3% increase, climbing from $12.2 million to $30.6 million.

-

Zenith Insurance Company: 63.9% growth, up from $90.6 million to $148.6 million.

These gains point to aggressive expansion and increased market penetration, particularly among foreign-owned insurers scaling their Canadian presence.

Beyond these leaders, several niche and specialty players posted double-digit revenue increases, reflecting growing demand in commercial lines, reinsurance, and tech-enabled underwriting strategies.

Revenue Declines Worth Noting

While many insurers posted strong gains, others experienced notable year-over-year declines in reported revenue. Whether due to portfolio repositioning, strategic withdrawal from certain lines, or broader market shifts, these changes are worth watching:

-

Royal & Sun Alliance Insurance Company of Canada reported a 64% decline in revenue, falling from $637.8 million to $229.8 million

-

SiriusPoint America Insurance Company dropped 60%, from $17.7 million to $7.1 million

-

The Nordic Insurance Company of Canada saw a 57.5% decline

-

Verassure Insurance Company and Unifund Assurance Company also recorded drops above 40%

While some of these may reflect intentional restructuring or divestment, others could signal the impact of a more competitive or softening market. Monitoring whether these trends continue into 2025 will help distinguish between temporary contraction and longer-term repositioning.

Top 20 by Growth Year over Year

Get the Data Behind the Graphs

We’ve compiled publicly reported OSFI data into accessible formats for deeper analysis for all companies that report.

Available to subscribers:

• Revenue by insurer

• Other income and expense breakdowns

• Net income comparisons

Designed to support industry professionals, researchers, and anyone digging into the numbers.

Sector Breakdown

-

Domestic Insurers generated $69.62 billion in revenue and $6.50 billion in net income. Their scale, diversified product offerings, and established market positions continue to drive steady performance.

-

Foreign Insurers, while contributing a smaller share of total revenue at $17.32 billion, reported $3.04 billion in net income. This accounts for nearly one-third of industry profits on just one-fifth of the revenue base, highlighting strong efficiency and profitability in targeted lines.

This balance between volume and efficiency illustrates a market where both broad-based and focused strategies can succeed. Foreign insurers often excel through lean operations and specialty focus, while domestic players benefit from distribution reach and underwriting depth.

Companies like Northbridge, Definity, and Certa continue to rise steadily across multiple metrics, signaling a competitive middle tier that is closing the gap with larger incumbents.

Top 20 by Net Income

Strategic Observations

-

The rollout of IFRS 17 continues to bring clarity to underwriting results, with insurers adapting well to the added transparency.

-

Profitability remains strong across both domestic and foreign insurers, suggesting balanced market dynamics.

-

The revenue and profit growth among emerging players and niche reinsurers may indicate future shifts in competitive positioning.

Outlook

With 2024 closing on a high note, the Canadian P&C sector is entering 2025 with considerable momentum. Continued investment in digital transformation, expansion strategies by global players, and operational efficiencies are likely to shape the year ahead. Regulatory stability and strong capital positions suggest the industry is well-prepared for whatever comes next.

Subscribe for free to access the full results, rankings, and additional tools that can help you stay informed and competitive in Canada’s evolving insurance landscape.

Want to Access More In-Depth Company Data?

Subscribe to gain free access to exclusive data, valuable insights, and upcoming powerful tools!

Explore detailed company data and trends

Receive exclusive industry insights

Get access to upcoming powerful tools

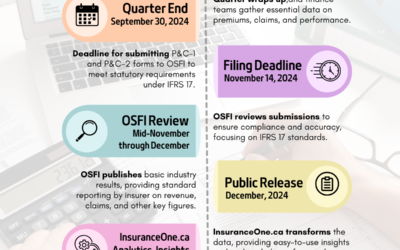

Navigating the OSFI Q3-2024 Filing Process

Today, November 14, marks the official OSFI Q3-2024 filing deadline for Canadian property and casualty (P&C) insurers, a critical milestone for...

What Are Your Predictions for Canada’s Q3-2024 P&C Insurance Results?

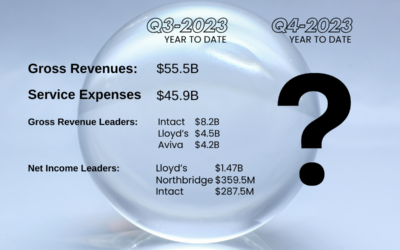

With Q3-2024 results from OSFI-regulated insurers on the horizon, it’s a great time to reflect on last year’s Q3-2023 year-to-date performance in...

Canada’s Top 10 P&C Insurers: First Half 2024 Year Over-Year Growth Leaders

The Q2-2024 results highlight the resilience and growth potential within Canada’s Property & Casualty (P&C) insurance sector. Leading the...

Canada’s Top 10 P&C Insurers: Q2 2024 Profit Leaders

The Q2-2024 results underscore the financial strength of Canada’s Property & Casualty (P&C) insurance sector, with total net profits after...

Canada’s Top 10 P&C Insurers: Q2 2024 Revenue Leaders

As of Q2 2024, Canada’s Property and Casualty (P&C) insurance industry achieved substantial revenue growth, reaching a year-to-date total of...